Menu

Menu  Search

Search

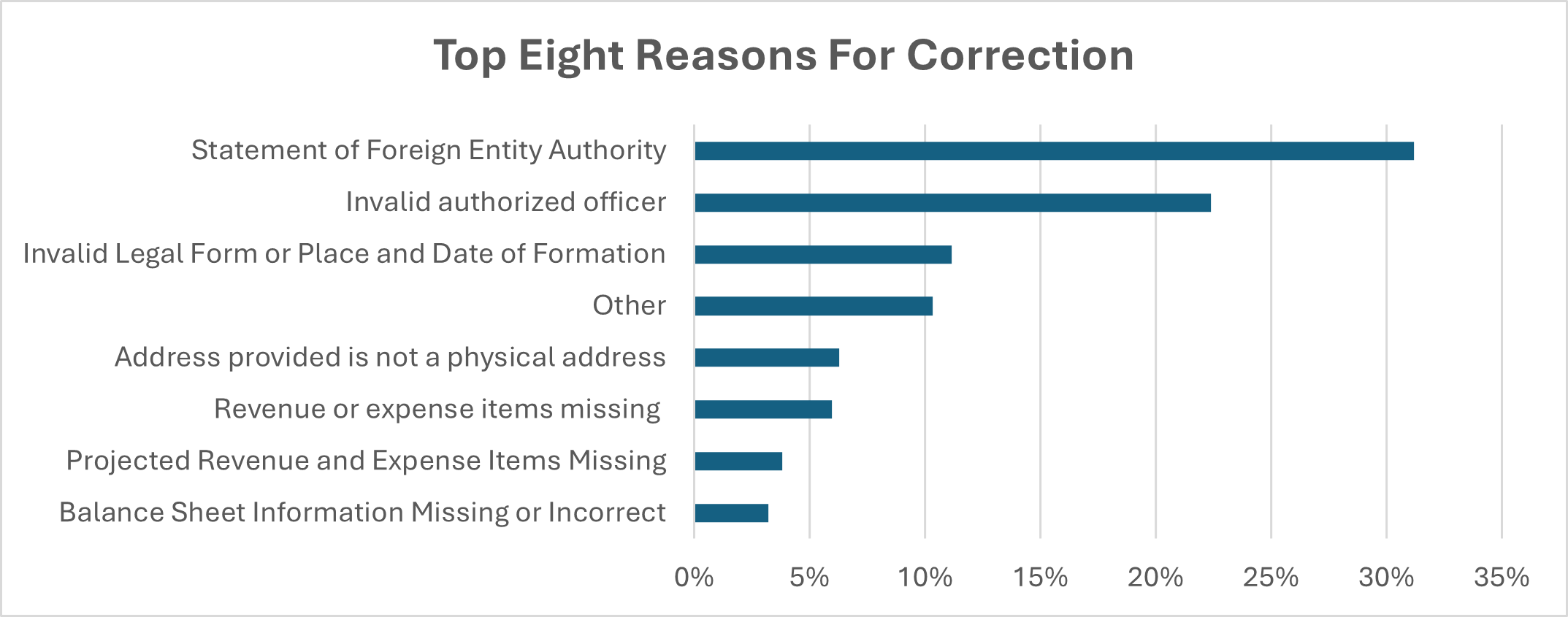

1. Statement of Foreign Entity Authority (31.19%)

An out-of-state entity needs to complete the Statement of Foreign Entity Authority (SOFEA) registration in the business filing system prior to approval for the charity registration.

Foreign Entity filing is the correct place to begin.

- Statement of Foreign Entity Authority instructions

- Foreign (outside of Colorado) entity filings

- File a Statement of Foreign Entity Authority online

2. Invalid authorized officer (22.40%)

An "authorized officer" must be an officer of a nonprofit corporation, a trustee of a charitable trust, or a senior manager member of any other entity subject to the filing requirements of the Colorado Charitable Solicitations Act. The authorized officer is also considered the account manager. An example of a role that is not an “authorized officer” is a third-party service provider that helps organizations with state registration. The e-file application features separate login credentials for preparers who can enter data but cannot submit filings by themselves.

3. Invalid legal form or place and date of formation (11.16%)

The Colorado Charitable Solicitations Act requires that all organizations disclose the place and date when they were legally established and the form of their organization.

If the organization was incorporated in Colorado, they may confirm the date of incorporation by searching the database.

If the organization is not incorporated, then please enter the form (type) of the organization as it exists under state law. Examples of formation types that could be included but are not limited to are "unincorporated nonprofit association", "limited liability company", "LLC", "charitable trust", "cooperative association". Please do not enter "charity", "charitable", "charitable nonprofit", "foundation", or similar terms. Don't enter IRS designations, such as "501(c)(3)".

4. Other (10.32%)

Rejections that don’t fit neatly into categories. For example, an error in the name of the organization or incorrect EIN.

5. Address provided is not a physical address (6.27%)

The Colorado Charitable Solicitations Act and the Rules for the Administration of the Colorado Charitable Solicitations Act require all registrants to provide the principal place of business of the organization. “Principal Place of Business” means the street address of the organization’s usual place of business and does not include a post office box or private mailbox. See section 6-16-104(2)(b), C.R.S. and 8 CCR 1505-9, Rule 1.15.

A P.O. Box, private mailbox vendor, or other mailing address may be entered in addition to a street address, but it cannot substitute for one, not even in mountain and rural communities.

If the organization in fact has no street address, it may provide the street address of its registered agent in Colorado, or if all else fails, it may list the street address of the officer who has custody of the organization’s corporate and financial records.

6. Revenue or expense items missing (5.96%)

One frequent reason for returning a document is a failure to list any revenue or expense items on the financial statement. It would be unusual for this to be a complete and accurate depiction of the financial activity of the organization.

If the organization in fact had $0.00 in revenue and expenses during the reporting period, please send an explanatory email to charitable@coloradosos.gov prior to filing the document.

7. Projected revenue and expense items missing (3.82%)

Organizations that are recently established will provide a projected first year budget made up of estimated figures (revenue and expenses) for their upcoming reporting period. This type of reporting could include but is not limited to administrative expenses such as charities registration filing fee and the tax-exempt application to the IRS. At the conclusion of the reporting period via an amendment filing, the organization will update the estimated figures to actual financials as part of the financial statement.

8. Balance Sheet Information Missing or Incorrect (3.21%)

Based on the revenue and expenses listed in this filing and balance sheet information available from a previous period, it is highly unlikely that the assets and liabilities listed in this filing are correct.